The Opportunity:

Saskatchewan, Canada

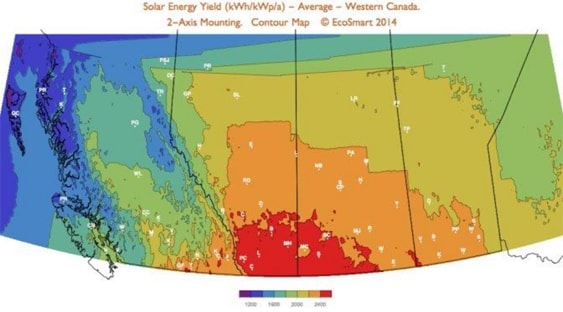

- The Southern Saskatchewan region receives the most sunshine in Canada.

- Saskatchewan has committed to reducing its dependence on coal fired plants for electric power from 72% down to 50% by 2030.

- A financial opportunity exists that combines tax credit advantage with charitable contribution through renewable energy investment. By partnering with Osborne Power you are provided an opportunity to invest in a safe, verifiable and predictable, federal government program.

Average Solar Energy Yield

Federal Government Opportunities

Renewable energy projects such as this are eligible for accelerated capital cost write downs.

- 50% accelerated capital cost reduction

Accelerated Capital Cost Allowance for Clean Energy Generation

A 50 percent accelerated capital cost allowance (CCA) is provided under Class 43.2 of Schedule II to the Income Tax Regulations for specified energy generation equipment. Eligible equipment must generate either (1) heat for use in an industrial process or (2) electricity, by:

- Using a renewable energy source (e.g. wind, solar, small hydro),

- Using waste fuel (e.g. landfill gas, manure, wood waste), or

- Making efficient use of fossil fuels (e.g. high efficiency cogeneration systems).

federal government opportunities

The guide provides information concerning the CCA classes in the Regulations for clean energy generation and energy conservation equipment;

- lists the types of property that are eligible and ineligible for inclusion in Class 43.1 or Class 43.2; provides schematic diagrams of the common types of qualifying systems;

- provides tables that list the types of costs that may be incurred for qualifying Class 43.1 or Class 43.2 property; and provides the application forms to be completed by taxpayers to request a technical opinion from Natural Resources Canada as to which assets in a planned or completed project may qualify for inclusion in Class 43.1 or Class 43.2.

Flow-Through Shares

- In return for the investment a flow-through share is produced in the amount of the investment. The initial investment is then used to purchase qualifying equipment that can be written down at 50% per year for three years. On a $10,000 investment, the flow-through shares would be issued as follows.

- Year 0 - $10,000

- Year 1 - $5,000

- Year 2 - $2,500

- Year 3 - $1,250

- A $10,000 flow-through share would produce $18,750 for every $10,000 invested.

charitable donation

Flow-Through Shares

- There is a further opportunity to take the flow through shares and donate them to a charity of your choice. The charity would issue a tax receipt for 80% of the share value.

- Year 0 - $8,000 charitable receipt

- Year 1 - $4,000 charitable receipt

- Year 2 - $2,000 charitable receipt

- Year 3 - $1,000 charitable receipt

- The combined flow-though share and charitable flow through share would result in $33,750 of tax benefit for every $10,000 invested.

Next Steps

Contact Colin to discuss how our flow-through partnership could work for you

As an investor you would provide the opportunity details to your financial adviser to confirm that this investment vehicle is right for you!

Upon confirmation, the investor and Osborne Power would enter into a contractual agreement wherein the funding is provided upon receipt of the Power Purchase Agreement. Once the funds are confirmed the flow-through share paperwork is issued.

The mature share is then sold, through a partner agency, to a registered charity(ies) of your choice. The charitable organisation issues you a tax receipt equivalent to 80% of the value of the flow-through share you purchased. This process is repeated for the next three years, as per the accelerated capital cost reduction program.

Director

Colin Osborne CRSP, CHSC

In his many years in resource-based industry, Colin Osborne has been inspired by innovative technologies employed to reduce the negative impact on the environment. The resource-extraction world is working hard to find the balance between supporting the need for fossil fuels, a solid economy for Canada, and shifting to renewable energy to meet Canada's commitments to climate control.

While working on his MBA Colin began to research these opportunities and became aware of federal government incentives. Private citizens and business would be incentivized to invest in renewable energy projects. These investments also have the added benefit of being transferred to charities under a similar federal government program.

Colin continues to operate his safety company and has worked in that field for the last twenty years. By partnering with companies and individuals who subscribe to the socially responsible, sustainable work process and methods Colin has been able to research and develop and grow more opportunities. Projects that he and Osborne Power are excited to share and grow with similarly motivated individuals and companies.

Current Partners in Saskatchewan

- Homelife Prairies Realty (Regina)

- Sound Solar Systems (Regina)

- Canada Imperial

Bank of Commerce (CIBC)

Links

This link http://www.nrcan.gc.ca/energy/efficiency/industry/financial-assistance/5147 is from the government regarding the schedules and requirements that the project must meet. Pay particular attention to pages 92-97 of http://www.nrcan.gc.ca/sites/www.nrcan.gc.ca/files/energy/pdf/Class_431-432_Technical_Guide_en.pdf where the details, construction and design is laid out in order for the project to qualify for the program.

The flow- though share agreement information can be found here http://www.cra-arc.gc.ca/tx/bsnss/tpcs/fts-paa/nvstr/hw-eng.html There is some really good information about the structure of the agreement. In particular about the carry forward of the share to best suit the investors individual needs. http://www.nrcan.gc.ca/mining-materials/taxation/8874

Projected Timeline (in weeks)

Week 1

- Agreement Terms & Conditions

- Area Permit Applications

Week 2-5

- Area Permit Applications

- Submission of Small Power Producer Documents to SaskPower

- Processing of Small Power Application

Week 6

- Agreement Terms & Conditions

Week 5-8

- Equipment Procurement

- Onsite Mounting/Foundations Layout Installation

Week 8-12

- Onsite Mounting/Foundations Layout Installation

- Small Power Producer Contract Arrival

Week 12-16

- Onsite Mounting/Foundations Layout Installation

- Onsite AC Wiring Installation

Week 16-22

- Onsite Mounting/Founadations Layout Installation

- Onsite Solar Panel Installation

- Onsite DC Wiring Installation

- Onsite Invator Installation

- Onsite AC Wiring Installation

Week 20-22

- Small Power producer Contract Arrival

- SaskPower Inspection

- System Commissioning